A discussion from an independent advisor / broker perspective

INTRODUCTION.

The financial services industry has been under a load of pressure over the past few years. This is often attributed to the financial crisis of 2008 that the financial services and more specifically the banks were blamed for. It was inevitable and understandable that a barrage of regulation had to follow that regrettably included the insurance broking and financial planning sectors equally hard as it did the banking sector. There can be no doubt that increased regulation brought with it increased cost.

But, it would be incorrect to attribute the magnitude of regulatory compliance merely to the financial crisis and developments since 2008.The FAIS Act was long in the making before it was enacted in 2002 and implemented in 2004. During these developing years it became abundantly clear that the FAIS Act would place stringent regulatory requirements on the insurance and advisory sectors and that compliance with it would result in significant costs, especially for the independent advisors and brokers.

THE COST OF COMPLIANCE.

“The cost of compliance” to my mind is a misnomer, especially from the perspective of the insurance and financial planning sector. It distracts from ascertaining the real cause, origin or source of any such expenditure. The central premise of this presentation is that compliance per se costs one nothing. It is only once one determines the actual cause, origin or source that contributes to being compliant that a debate about the cost of compliance becomes meaningful.

To develop this approach further I would like to refer to an interesting article by Valerie Hayter in the November 2013 issue of Cover magazine, in which she explores the setting-up costs of a UMA with reference to operational and financial considerations. Two considerations that she highlights are as follows:

- Income / revenue. In the insurance broker / financial planning sector this is normally commission and allowable fees.

- Expenditure. The primary expenditure is operating costs that may vary depending on the type of business, operating structures automation and staffing.

“… Other expenditure elements include accommodation, administration (office running expenses, audit and compliance) IT costs, marketing and travel.”

What I found interesting is the inclusion of compliance cost as an integral part of total operation costs. I will touch on this point again later on.

DEVELOPING THE CENTRAL PREMISE OF THIS PRESENTATION.

To develop the suggested premise or approach for this presentation it is necessary to explore a few concepts / definitions. (Reference: The Concise Oxford Dictionary.)

Compliance. The act or instance of complying; obedience to a request or command, i.e. what is expected and / or acceptable.

Comply. Act in accordance with a wish, command or expectation.

Essence. The indispensable quality or element identifying a thing or determining its character or fundamental nature.

Essential. Absolutely necessary or indispensable.

Inherent. Existing in something, a permanent or characteristic attribute.

Innovate. Bring in new methods, ideas or make changes.

Regulate / regulation. Control by rule or subject to restrictions or an authorative directive.

Applying the definitions to the topic of this discussion.

- Compliance in the insurance broking / financial planning environment is first and foremost driven by the client’s expectations. To comply then means to act in accordance with those wishes and expectations. There is no immediate implication of obedience to a command and thus no immediate censure. It is rather an attitude to want to meet the client’s expectations. It entails doing the right thing, for the right reason, at the right time with due care and diligence to obtain the expected outcome. This is the essence of acting in terms of one’s fiduciary duty towards the client! This attitude or mindset does not in itself “costs” anything. The real cost of non-compliance will most certainly lead to a loss of a client and thus loss of business.

- Compliance is essentially a “DO” function. The attitude must be there but to comply means to “act in accordance” and is therefore dependent on the way or manner in which something is done, i.e. the process.

The process is dependent on how it is done, i.e. procedures methods and activities, the timing of execution and completion as well as with what, i.e. equipment, aids and monetary resources.

- Regulation is not an inherent characteristic of compliance but nevertheless sometimes necessary. It is however unfortunate that statutory regulation inevitably results in significant ‘add-on” or introduced costs.

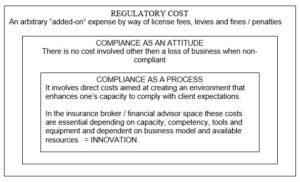

THE COMPIANCE / COSTS MODEL

DISCUSSION.

It is a fact that financial services regulation, with specific reference to the insurance broker / financial planning sector mainly focuses on market conduct (including best practice and treating customers fairly) and (future) regulation of income streams, The intention is to not only debate the necessity thereof but also to look into the cost implications thereof.

The model given above aims to demarcate where exactly in compliance costs apply and / or originate. Applying the definitions quoted earlier it should be quite clear that compliance does not lead directly to any cost that would not have been incurred anyway. The main source or reason for specific costs and expenditure is firstly the process to comply.

Especially in the case of the broker / advisor this is costs or expenditure one would direct towards enhancing one’s own ability to be compliant, i.e. to best meet the needs and expectations of one’s client. It is cost incurred to develop the own competitive edge and in doing so to ensure the growth and stability of one’s business.

My experience since the advent of FAIS in 2004 is that for many of my clients it was absolutely necessary to incur some such costs, admittedly to a higher or lesser degree, just to stay competitive. In an industry where especially technological advances and ever changing consumerism dictated change, this lead directly to a high level of innovation!

Unfortunately, this necessary expenditure was by many seen as costs to be incurred because of the implementation of FAIS and other consumer / market conduct legislation and regulation. This is of course not the case but it does bring to the fore costs dictated directly by statutory regulation and compliance with it. This now opens a completely different debate or argument that can be discussed namely;

- The appropriate level of regulation.

- The direct costs of regulation, e.g. licensing, fees and possible penalties.

REGULATION AND COSTS.

Regulation in terms of different legislation has been with us since the early parts of the 20th century, including regulations regarding various aspects of the economy. Examples thereof are the exchange control (Currency and Exchanges Act; 1933) the Short-term and long-term Insurance Acts, FICA and related legislation as well as tax legislation, e.g. VAT. As stated previously, statutory regulation is not in itself undesirable but one thing that stands out is the magnitude and extent of regulation affecting the financial services industry.

The effect of this sometimes “over regulation” is that it carries a cost. Not only a direct cost to players in a certain field but to business and the economy at large. It is becoming ever more difficult to do business and to offer the best rates / prices to consumers.

One aspect that no doubt affects the cost of regulation is the current approach to regulation of a broad brush, one-size-fits-all approach. This is especially true of the broker / advisor environment and insurance industry as a whole, especially as is evident under FAIS regulation. This “lowest denominator” approach is especially evident under FAIS. The application of sometimes very stringent regulations takes very little notice of amongst others:

- The nature of the entity and its product delivery.

- The nature and the risk that the entity’s client base is exposed to in the event of not complying with specific regulatory aspects.

- The actual role or involvement of entities in certain regulatory desired outcomes. TCF is a prime example.

A question that is often raised is whether an Act that mandates a government or statutory regulator, like the FSB to vary the application of an Act by means of drafting regulations to the Act is constitutional? With reference to the cost that is directly or indirectly associated with regulation it can be questioned whether the consumer is better off in terms of affordability of services? (For a detailed discussion of this topic refer to an article by Dr. Gerrit Sandrock in the January 2014 issue of Cover magazine.)

WHAT IS THE TRUE COST?

There is no actual cost to compliance. The cost will depend on expenditure required for self enhancement or innovation to stay compliant and may include some costs to put in place measures that will in any case enhance one’s own ability. My experience is that some of my clients had to spend more on this than others depending on their initial readiness to adopt best practice.

On the other hand the reasons and extent of regulatory directives should be critically evaluated in terms of necessity, applicability and unforeseen consequences. Once this is done then the cost to comply as imposed directly by any Regulator can, and needs to be addressed.

I conducted an analysis of the cost of compliance amongst my clients, who mainly include long-term and short-term insurance brokers, employee benefit and investment advisors. These entities vary from “one-man” to large corporate intermediaries.

Included in the analysis were the following items and respondents had to express their expenditure as a percentage of gross income; i.e. commission and allowable fees.

- Direct compliance and regulatory costs; licensing, fees, penalties, etc.(In only one case did this involve a settlement with the client after a complaints resolution process.)

- Expenditure on continued professional development.

- Cost of innovation; to enhance procedures and methods, communication, etc

- Cost of resources; IT and equipment.

Preliminary Results.

In one instance, the entity being a short-term UMA the figures were given as a % of overheads. (Defined as expenditure arising from general running costs.)

| Underwriting Management Agency (Binder Holder) | |

| Direct compliance and regulatory costs; licensing, fees, penalties, etc | 2.5 |

| Expenditure on continued professional development. | 1,0 |

| Cost of innovation; to enhance procedures and methods, communication, etc | 0.5 |

| Cost of resources; IT and equipment. | 4.0 |

| Total | 8.0 |

| It is interesting to note that the cost associated with upgrading of IT systems is significantly higher with direct compliance / regulatory cost the next highest. | |

Something that was also interesting up to the time of writing this presentation is the figures for my three biggest clients. One is a large long-term insurance broker on risk only products with multiple sales offices and a small short-term division. One is a large short-term broker on both personal and commercial lines, including a call centre. The third (given below) is a family owned medium-large broker with both a short-term and long-term division that also advises on investment products. As regards my two biggest clients the total figure came to about one percent of annual income.

Cost given as % of gross income; i.e. commission and fees.

| Family owned medium-large short and long-term broker, including investment advice. | |

| Direct compliance and regulatory costs; licensing, fees, penalties, etc | 0.13 |

| Expenditure on continued professional development. | 0.35 |

| Cost of innovation; to enhance procedures and methods, communication, etc | 0.70 |

| Cost of resources; IT and equipment | 0.22 |

| Total | 1.4 |

The following gives the result of a family owned long-term and short-term insurance broker with a large medical-aid component.

| Family owned medium size short and long-term broker with medical aid | |

| Direct compliance and regulatory costs; licensing, fees, penalties, etc | 1.1 |

| Expenditure on continued professional development. | 2.2 |

| Cost of innovation; to enhance procedures and methods, communication, etc (In this case the entity invested in a complete operating system to satisfy CMS) | 3.8 |

| Cost of resources; IT and equipment | 4.5 |

| Total | 11.6 |

The following gives the results of a single member / shareholder short-term insurance broker

| Single owner, Short-term broker on personal and commercial lines | |

| Direct compliance and regulatory costs; licensing, fees, penalties, etc | 2.9 |

| Expenditure on continued professional development. | 3.0 |

| Cost of innovation; to enhance procedures and methods, communication, etc (In this case the entity invested in a complete operating system after having moved away from a traditional short-term administrator) | 5.0 |

| Cost of resources; IT and equipment | 5.3 |

| Total | 16.2 |

I think that the above case illustrates the tremendous sacrifices that small brokers have had to make to comply with regulatory requirements, notwithstanding that the entity has been in business since long before the FAIS act was implemented with a steady client base.

What needs to done however is for the Regulators to decide on the optimum levels of regulation for different services providers in terms of costs and risk to consumers and to adapt regulatory requirements to each type of intermediary, difficult as it may be.

Robbie Stutterheim.

Compliance officer.

Robert J Stutterheim Consulting